What Does the Stock Market Tell Us about the California Wildfires?

What Does the Stock Market Tell Us about the California Wildfires?

17 January 2018

Published by https://energyathaas.wordpress.com/

USA – California utilities have lost $20 billion in market value since the wildfires began.

The horrific wildfires in Northern California’s Wine Country in October and then in Southern California in December killed more than 40 people, burned 1.2 million acres, destroyed thousands of buildings, forced hundreds of thousands to evacuate their homes, and led to deadly mudslides.

From the beginning investigators have focused on power lines as a likely cause. And, as more evidence becomes available, it continues to point to power lines. For example, the San Francisco Chronicle now reports that damaged electrical equipment was found at or near the suspected ignition points of four of the biggest wildfires in Northern California.

It will be some time before these investigations have concluded, but it is not too early to begin to assess the stock market fallout. How has the stock market reacted to this news? What does this mean for California electric utilities? For shareholders? For utility customers?

PG&E Tumbles

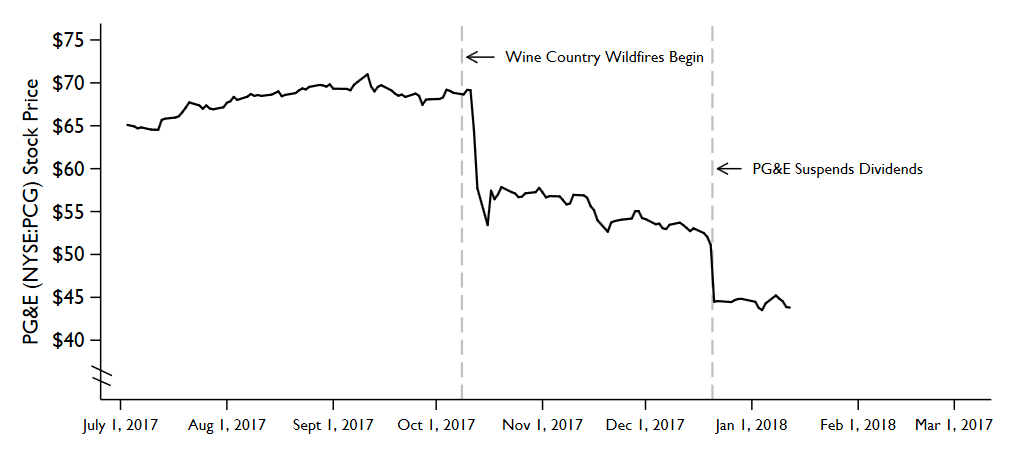

Pacific Gas and Electric (PG&E) has been the hardest hit. Before the wildfires began, PG&E stock was trading near $70 and the company was worth $36 billion. The selloff started shortly after the wildfires began on October 8thand by mid-October PG&E’s stock had tumbled to near $55.

Source: Constructed by Lucas Davis at UC Berkeley.

Source: Constructed by Lucas Davis at UC Berkeley.

Then on December 20th, PG&E announced it would suspend its dividend program due to looming potential fire liability, leading to another selloff and stock prices falling to $45. Companies are generally loath to cut dividends because it is perceived by the market to be a very bad signal.

Since October, PG&E’s market value has fallen by $13 billion. This 37% drop reflects potential liability from the more than 50 lawsuits that have been filed against PG&E, representing hundreds of families and businesses who have suffered damages from the wildfires. With the number of lawsuits continuing to grow, PG&E’s total liability could easily exceed the $800 million in liability insurance held by the company.

Edison Plummets

Southern California Edison followed a similar pattern. Before the Southern California wildfires, Edison’s stock was at $80 and the company was worth $26 billion. When the wildfires began, Edison’s stock price immediately plunged 16% with shareholders concerned that, like PG&E, the utility would be forced to pay damages. Since then, the stock has continued to slide with several lawsuits alleging that Edison equipment played a role in starting the fires. Overall, Edison’s market capitalization has fallen by $6 billion, almost one-quarter of its total value.

Source: Constructed by Lucas Davis at UC Berkeley.

Source: Constructed by Lucas Davis at UC Berkeley.

Broader Signal?

Interestingly, one of the worst days for Edison was December 21st, after PG&E announced it was suspending dividends. That day, PG&E stock went down 13%, while Edison stock fell 7%, so a smaller, but still very significant decrease.

I think I understand why PG&E’s stock went down. Companies like PG&E usually try to avoid cutting dividends, so it would make sense for the market to take this announcement as bad news, implying that PG&E’s liability was greater than previous believed.

But why did Edison’s stock go down? They are separate companies, separate wildfires, and separate investigations. Yet the market took PG&E’s announcement as a broader signal. Even San Diego Gas and Electric (Sempra Energy) went down the same day by almost 5%; a single-day loss equal to more than $1 billion. Did shareholders conclude that Edison and Sempra were also likely to cut dividends? Or did the PG&E announcement reveal something deeper about the prospects for all California electric utilities?

A related event got a lot of attention, but had little immediate effect on stock prices. On November 30th, the California Public Utilities Commission rejected a request from San Diego Gas & Electric to charge customers $379 million to cover costs from a 2007 fire. The decision was interpreted by the media as bad news for utility shareholders, but it had little immediate impact on stock prices. Neither SDG&E (Sempra), nor Edison, nor PG&E experienced any significant decline. Either the decision was already priced into stock prices, or it was deemed unimportant by the market.

What about Utility Customers?

In part, the size of the stock market reaction reflects a concern that even if the utilities did nothing wrong, they could be liable for significant damages. This could occur through “inverse condemnation” court cases, a concept that flows from the US and state constitutions and is closely related to eminent domain. Government and public utilities can obtain private property through eminent domain processes in which they compensate owners for the lost use of their property. If a government (or a public utility) damages private property and doesn’t compensate the owner, then the owner can bring an inverse condemnation case.

Utilities could try to argue that the damages they pay through inverse condemnation should be passed along to customers as part of the broader costs of providing electric service. But will utilities actually be able to pass along these costs? The market does not expect 100% of these costs to be passed on to ratepayers; otherwise you wouldn’t see these large stock market impacts. But there may well be rate increases. California legislators are introducing legislation that would prohibit the CPUC from pushing fire liabilities onto rates, but it is too soon to know what will happen with this legislation. The damages from the wildfires are very large. The Tubbs Fire and Thomas fires were the most destructive and largest fires in California history, respectively. So there is more than enough pain to go around.

Who Should Pay?

Many questions remain. Who should pay for wildfire damages? How do we incentivize utilities to reduce wildfire risk? How much risk should be borne by shareholders? By utility customers? What is fair?

A central tenet of law and economics is that agents should bear the costs of their actions. Utilities are constantly making investments in fire prevention and you want utilities to make these decisions efficiently, “internalizing” the potential damages from action and inaction. So you want shareholders to be liable, to have significant “skin in the game” so that their companies will take the right actions to reduce wildfire risk.

But at the same time, you also don’t want to make utilities responsible for all wildfire damages, regardless of whether the companies acted negligently. This would raise the cost of capital for utilities, making it hard for them to finance basic operations. Put simply, if you make it unattractive enough to be in the utility business, nobody will want to do it.

This is not just about power lines. With climate change average temperatures keep climbing, and the summer of 2017 was much warmer and dryer than usual. And California’s population keeps growing, with more and more people living in fire-prone parts of the state. The devastating California wildfires of 2017 raise many very difficult questions that we are going to be asking for a long time.